CLI Newsletter February,2026

After a cooling period in 2025, the Texas economy is entering 2026 with renewed momentum. While job growth hovered near zero last year due to labor supply constraints and an immigration crackdown, the outlook for 2026 calls for a 1.1% increase in employment. This growth is being propelled by a massive structural shift toward high-tech infrastructure and easing financial conditions.

Strategic Growth Drivers:

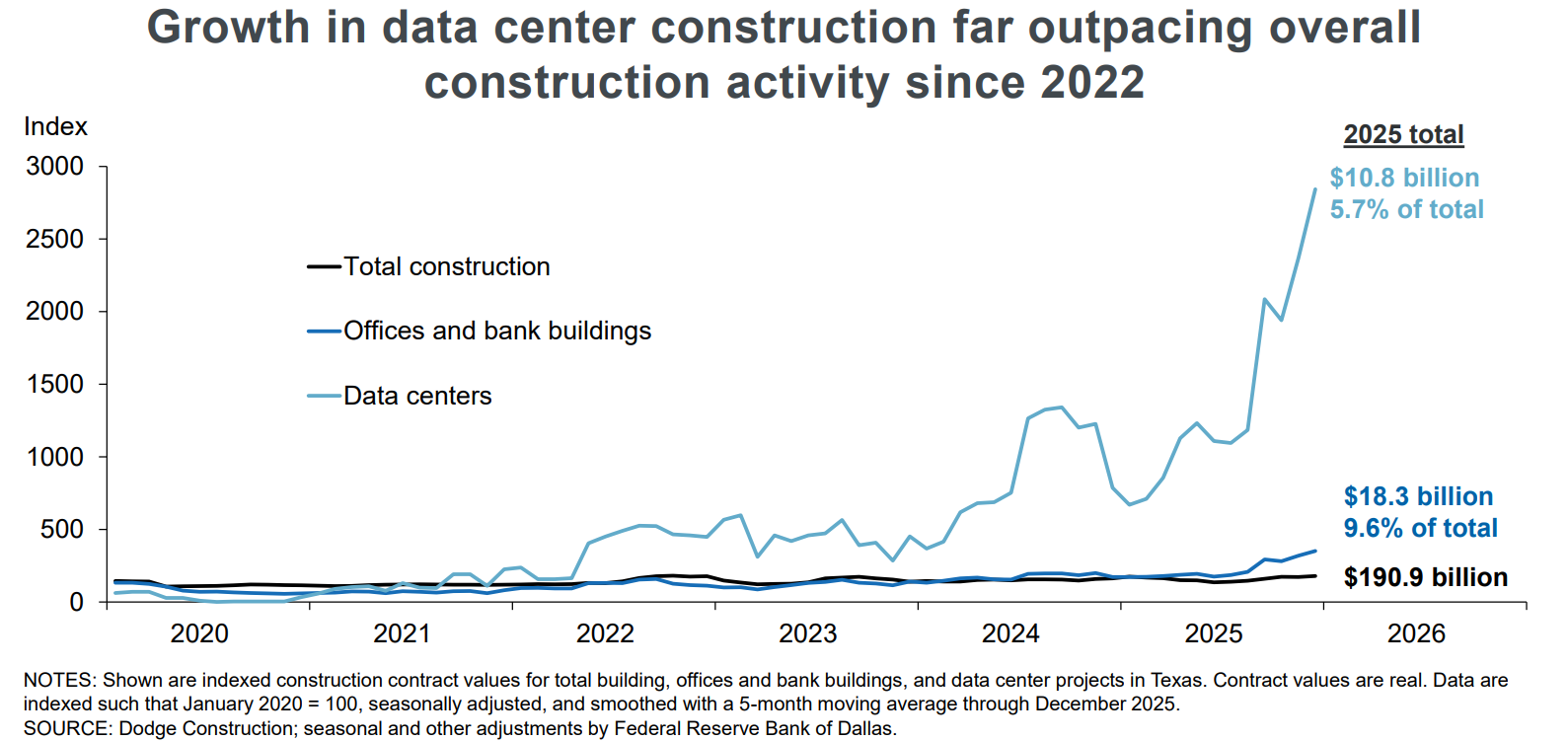

The High-Tech Infrastructure Pivot: Texas has decoupled from the national trend in office construction. Instead, it has pivoted to become the nation's second-largest data center market. Fueled by the AI boom, data center investment in Texas surged to $18.3 billion in 2025, representing nearly 10% of all construction value in the state.

Energy & Utility Resilience: Despite lower WTI oil prices (hovering around $60/barrel), the energy sector is shifting from pure extraction to infrastructure. "Non-building" construction—encompassing grid upgrades and energy utility projects—is at an all-time high, offsetting the slump in the residential sector.

The World Cup Catalyst: As we look toward the 2026 FIFA World Cup, the service sector is preparing for a massive influx of international capital and tourism. This event is expected to be a primary driver for the hospitality and retail industries, providing a unique cyclical boost to the state’s GDP.

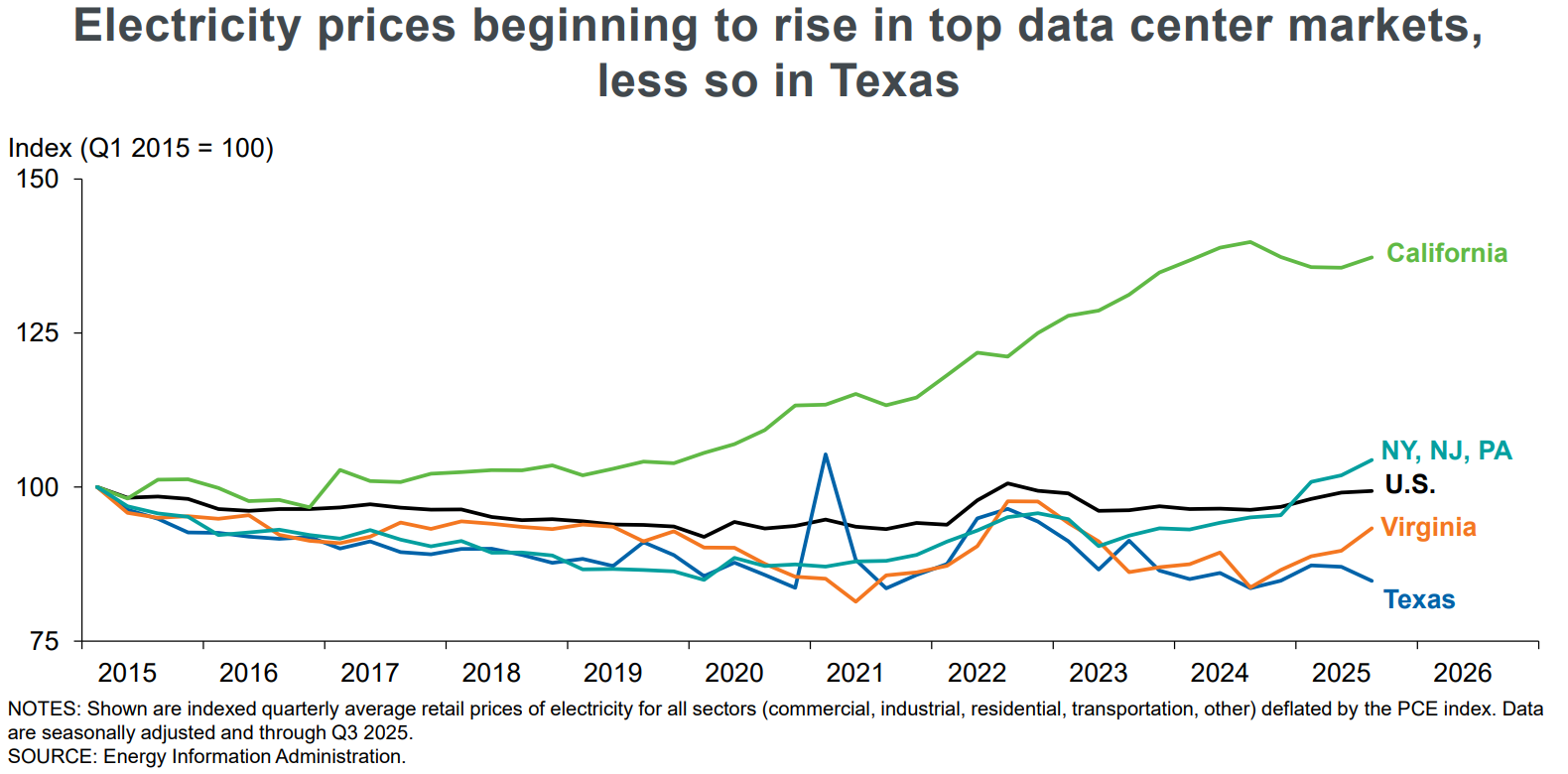

Competitive Cost Advantage: Even as power demands soar, Texas maintains a significant electricity price advantage over other tech hubs like California and Virginia. This "energy delta" continues to attract heavy-industrial and tech firms looking to escape the rising operational costs of the East and West Coasts.

At the conclusion:

Texas grew in 2025 without adding jobs—this hasn’t happened since the jobless recovery of 2002-2003!

Despite this, there are few signs of broad-based labor market slack; the headline unemployment rate remains low and stable.

Job growth is expected to pick up in 2026, though the recovery will be mild.

Productivity gains are suppressing hiring, while the immigration crackdown is significantly limiting labor supply.

A continuing AI boom and OBBBA tax provisions will likely boost activity, while low oil prices and a residential construction bust remain primary drags on growth.

The FIFA World Cup will provide an additional cyclical boost to the service sector.

Other concerns to monitor include safety net cuts and federal funding reductions, particularly in health care and education.

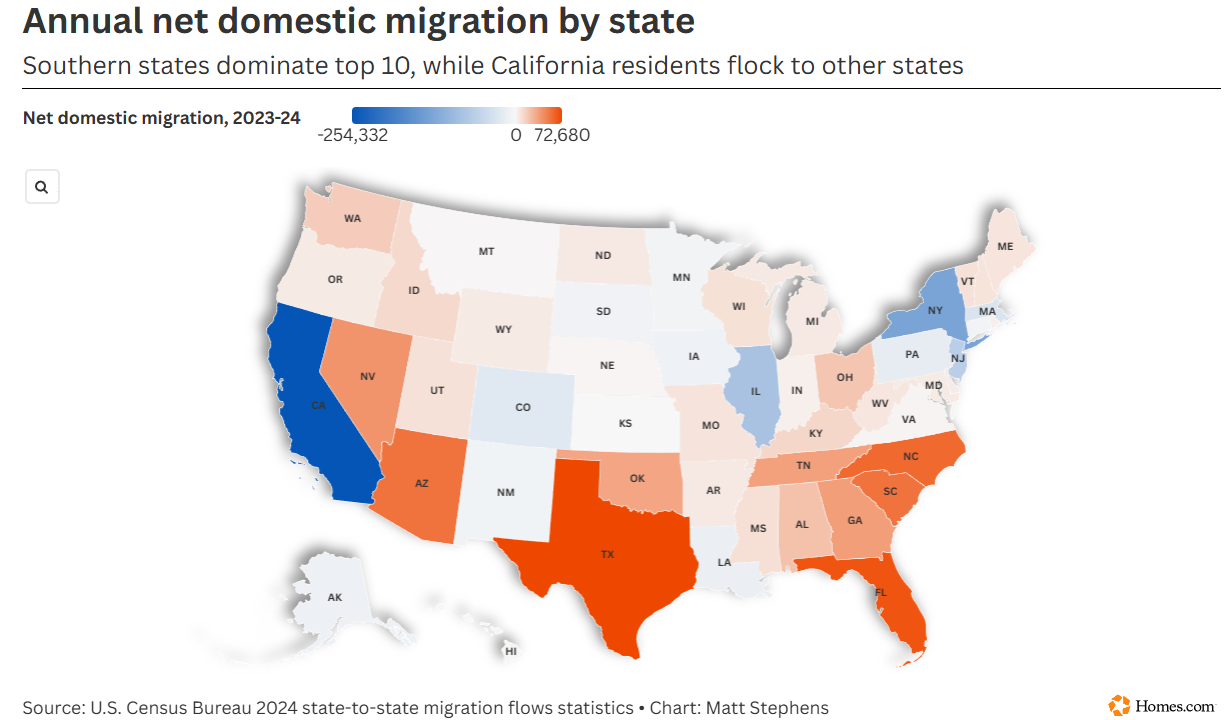

The great American migration shift continues to favor the Sun Belt in 2026. According to the latest U.S. Census Bureau data, Texas and Florida have secured the largest spikes in state-to-state migration, driven by a relentless search for better employment, lower taxes, and housing affordability. The South now accounts for all 10 of the top spots for net domestic migration, reinforcing its position as the nation's economic engine.

While Texas added tens of thousands of new residents from other states, California and New York saw the most significant losses, with California alone losing over 250,000 people. As Brad Case, chief residential economist for Homes.com, notes, this movement is fundamentally driven by financial and lifestyle optimization. For real estate investors, this sustained influx of "new Texans" provides a permanent tailwind for both multifamily and single-family rental demand, ensuring high occupancy rates in key metropolitan hubs like Dallas and Houston.

Why Build-to-Rent Is Shaping the Housing Market in 2026

Presented by Matthews

The Build-to-Rent (BTR) sector continues to assert itself as one of the most dynamic forces in U.S. residential real estate in 2026. As homeownership remains out of reach for many due to affordability pressures, BTR communities—single-family homes built specifically for long-term rental—offer the perfect middle ground for families seeking suburban layouts without the responsibilities of a mortgage.

A significant shift in 2026 is the consolidation of the market. While over 200 developers are active, the pipeline is increasingly dominated by a few major players like Taylor Morrison and Empire Group, who have the scale to secure financing in a tighter capital environment. With over 64,000 homes currently under construction and another 139,000 in planning, BTR is no longer a "niche" strategy. It is now a primary target for institutional capital, particularly in high-growth Sun Belt metros where migration continues to fuel a desperate need for high-quality rental supply.

UPCOMING OPPORTUNITY

The Samuel

The Samuel will be a 14-story, Class-A student housing tower located adjacent to Arizona State University’s Tempe campus.

At completion, the project will include 224 units with a total of 408 beds and 8,200 square feet of ground floor retail space.

Exclusive amenities to residents will include a rooftop pool, hot tub and basketball court, a fitness center, study and communal lounges, and sports lounge with outdoor terraces, as well as 24-hour onsite staff and concierge.

Positioned steps from Arizona State University (ASU) and Downtown Tempe, The Samuel is designed to serve the growing student population and capitalize on the strong demand for student housing within the Tempe market.

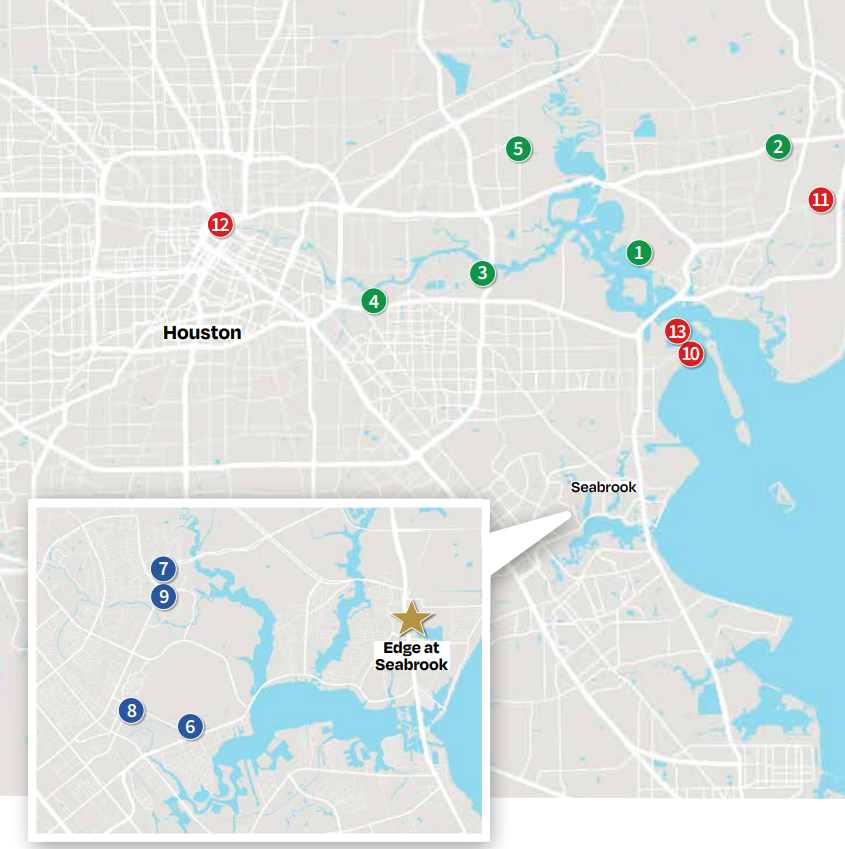

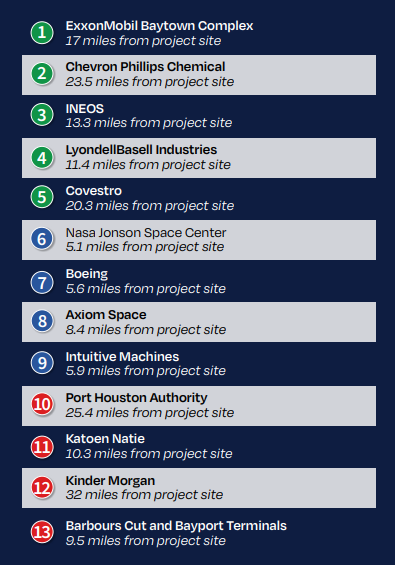

The Edge at Seabrook

The Edge at Seabrook is another premier investment opportunity from NHK, featuring a Class-A garden multifamily development located within the Seabrook Towne Center mixed-use community.

This investment funds the development and construction of a ~289,000 SF community with 320 units, anchored by nearby retail, restaurants, and lifestyle amenities. Residents will enjoy top-tier facilities including two resort-style pools, a clubhouse, pickleball courts, two fitness centers, and garage parking—all within walking distance of the Seabrook Town Centre.

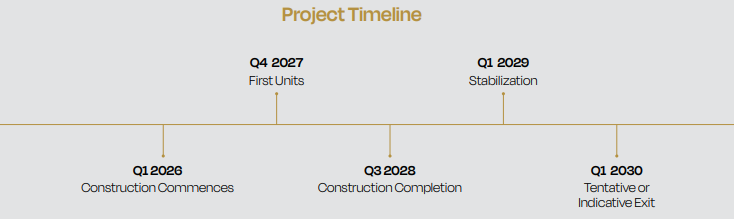

The groundbreaking ceremony was successfully completed on January 31, 2026. The project is currently on track for a tentative exit in Q1 2030.